Key takeaways

• Recent repricing in the high yield market presents attractive entry points and supports a constructive outlook.

• The high yield market is in a healthy state with solid company fundamentals and low defaults.

• In rising-rate environments, high yield bonds benefit from a shorter duration profile and tend to outperform.

• Amid volatile markets, we remain focused on idiosyncratic ideas and bottom-up security selection

Fixed income investors are facing a conundrum amid rising rates and heightened macro risks. The war in Ukraine and surging inflationary pressures add to the uncertainty. Despite the headwinds, we think three key factors support a constructive outlook on the high yield asset class.

#1 Recent repricing presents attractive entry points

Heading into 2022, the high yield bond market was a tale of two halves. On one hand, solid company fundamentals, balanced market technicals and the ongoing economic recovery painted a supportive backdrop. On the other, valuations reflected the rapid fundamental improvement and were historically rich, with tight spreads and low all-in yields.

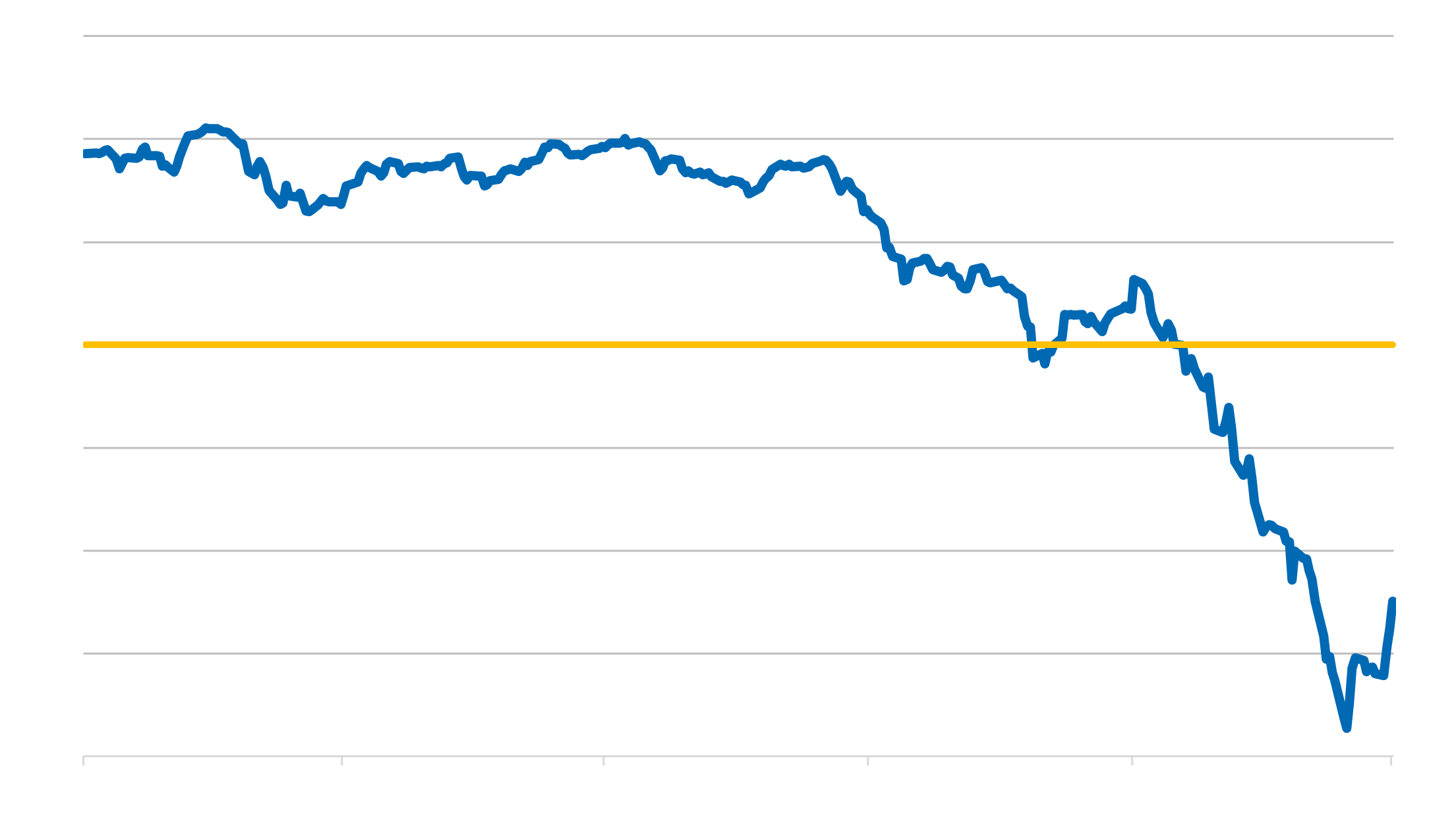

Now, valuations look more interesting. The broader risk-off tone across financial assets during 2022 has resulted in a repricing in high yield bonds this year. Notably, the yield to worst on the ICE BofA Global High Yield index is now above 6% (Exhibit 1) and the average bond price for the index has fallen to below par (Exhibit 2). The recent repricing now puts the asset class at the upper end of the one-year range. At these levels, valuations are more compelling and present attractive entry points.

Exhibit 1: Global high yield bond yields are above 6%

Exhibit 2: Global high yield bond prices are below par

#2 Healthy company fundamentals, low defaults

Despite the recent market weakness, high yield issuer fundamentals remain healthy. For most companies, earnings have returned to pre-pandemic levels and the pace of debt growth has slowed, resulting in declining leverage and improving coverage ratios. Liquidity is strong, with few near-term maturity wall concerns, and rating agencies are recognizing this fundamental improvement as credit rating upgrades outpace downgrades. The biggest concern we have is with inflationary pressures and the potential negative impact on margins, but so far we have been impressed with companies’ ability to increase prices.

Given the strong fundamental backdrop, US high yield default rates are at the lowest level since 2007 (Exhibit 3). Signs of distress are also limited. The percentage of high yield trading below $70 is also at the lowest level in years. Within European high yield, the trends are similar with below-average default rates and limited distressed situations. Looking ahead, we expect defaults to remain subdued given strong fundamentals, limited distress and supportive capital markets.

Exhibit 3: High yield defaults near historic lows; muted forecasts

#3 High yield tends to perform well in rising rate environments

Hawkish monetary policy from central banks is paving the way for rate hikes in 2022. While rising rates are a reason for concern for all fixed income markets, high yield bonds have historically performed well in these environments (Exhibit 4). This is because rate hikes typically coincide with strong economic growth in which corporate fundamentals are healthy and high yield companies are performing well. Further, high yield benefits from a short duration profile, which can help dampen the effects of rising rates. The higher spreads can also serve as a cushion since spread tightening can help absorb movements in rates.

Exhibit 4: High yield has historically performed well in rising rate environments

Uncertainty is opportunity

Amid the plethora of uncertainties and macro risks, markets will likely be choppy this year. While bouts of volatility and moments of spread widening are likely, we expect the high yield market to remain relatively resilient against a backdrop of solid fundamentals. Additionally, volatility can create opportunities for active managers to generate excess returns by avoiding problem credits and focusing on high-conviction ideas. During this environment, we are focused on bottom-up research and security selection as idiosyncratic ideas provide the best opportunities to generate excess returns.